- 1- How much do I need for a down payment?

- 2- Do I need a real estate agent, and what are the fees?

- 3- Can I back out after making an offer?

- 4- What are all the additional fees to consider beyond the purchase price?

- 5- Who pays the notary fees, the buyer or the seller?

- 6- Is mortgage pre-approval mandatory?

In this article, we answer 6 questions every buyer asks about down payments, choosing a broker, the purchase offer, closing costs, and mortgage pre-approval.

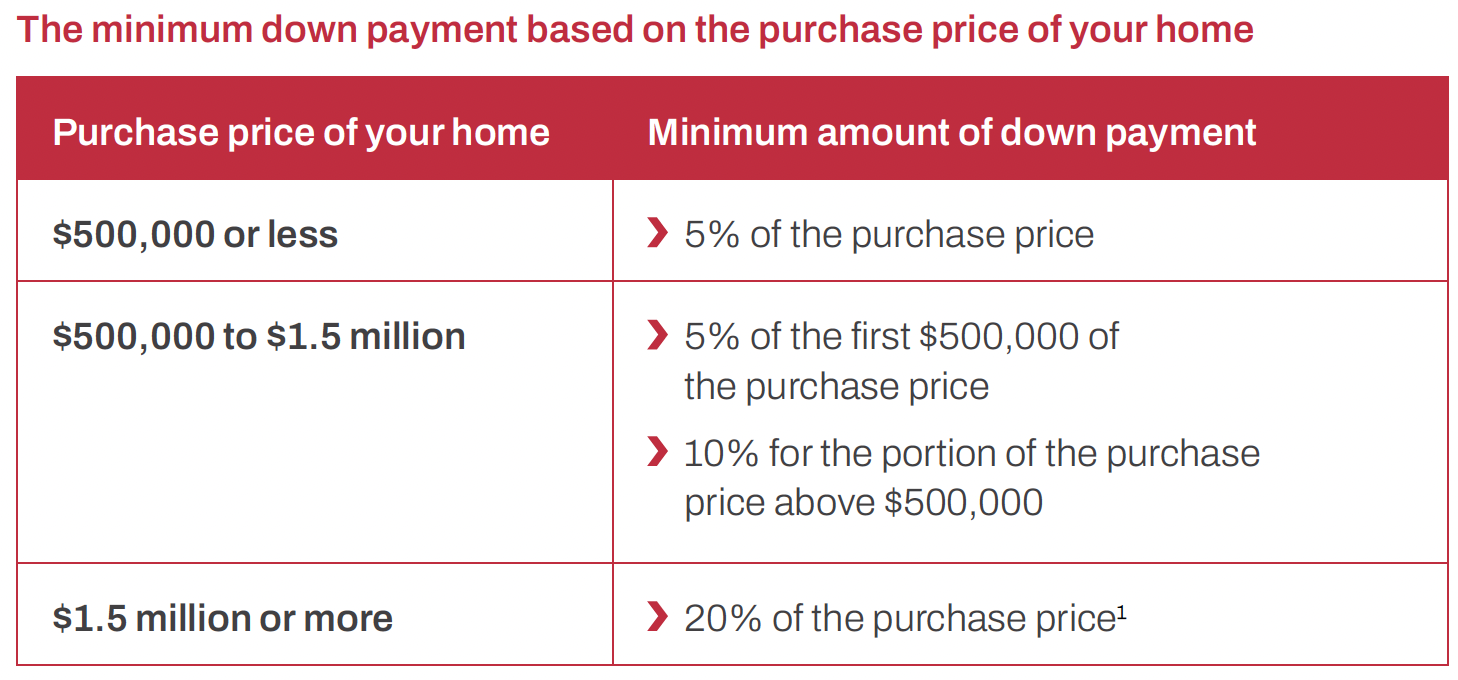

1- How much do I need for a down payment?

The million-dollar question.

First, analyze your assets, debts, and all types of financial goals (personal, family, and professional). It’s the best way to determine how much house you can afford. Then, with your mortgage broker, you can determine how much of a mortgage you can qualify for. Then, with your mortgage broker, you can determine how much of a mortgage you can qualify for. At this stage, you’ll decide how much of a down payment you can afford and need to put down.

The minimum amount you must provide as a down payment always depends on the home's purchase price. Here are the obligations:

Note that if your down payment is less than 20% of the purchase price, you will need to obtain mortgage loan insurance.

2- Do I need a real estate agent, and what are the fees?

No, it's not mandatory.

However, without a broker to represent you, your interests won't be protected during the process.

In a real estate transaction, a residential broker cannot simultaneously represent both a buyer and a seller under a brokerage contract with both parties, as their interests are in conflict. Double representation is forbidden under the Real Estate Brokerage Act. Buyers who choose not to be represented will still receive fair treatment from the seller's broker, who will exclusively defend the seller's interests and not those of the buyer.

What is the cost?

The OACIQ does not impose fixed commission rates. The compensation (commission) is an agreement that you negotiate with your broker and can vary from one agency or professional to another. It can take two forms:

- A percentage of the sale price (commission)

- A flat fee (fixed)

Who pays the commission?

As a buyer, if you have signed an Exclusive rrokerage contract – Purchase, your broker’s compensation is, in principle, your responsibility.

However, in most cases, if the seller is also represented by a broker, the latter offers a shared commission. The amount provided by the seller is then deducted from what you owe your broker under your contract. In such cases, the buyer typically does not have to pay any compensation directly.

3- Can I back out after making an offer?

Technically, no.

The promise to purchase is a contract. As soon as you submit your offer, you are committing to buy the house. You are therefore legally bound by the conditions attached to it. If either party fails to honor their commitment, they may face legal action for breach of contract.

Whether you decide to buy on your own or with the help of a Proprio Direct real estate broker, the legal implications are the same. That is why it is in your best interest to be well-supported by a broker. They ensure that your clauses provide adequate protection, helping you avoid mistakes that could cost you dearly.

ARTICLE : 8 essential things to know before submitting a promise to purchase

4- What are all the additional fees to consider beyond the purchase price?

Beyond the down payment, there are several additional costs to consider:

- Inspection

- Notary

- Home insurance

- Moving

- Renovations (if necessary)

- Annual fees

- Utility costs

- Condominium fees, if applicable

- Property maintenance

- Etc.

The Welcome Tax is reimbursed for first-time homebuyers

In the spring of 2026, the Government of Quebec announced that it will reimburse the welcome tax in the form of a tax credit for first-time homebuyers.

Key details:

- A full reimbursement of up to $5,000 in land transfer duties. For amounts exceeding this, you receive an additional credit of 25% on the remaining balance, up to a maximum of $875.

- Buyers who have not owned a home in the last 4 years. For couples, both individuals must meet this criterion.

- This measure applies to homes purchased since January 1, 2026.

To avoid any surprises, it is essential to consider all of these costs when planning your budget. We recommend setting aside approximately 1.5% to 3% of the purchase price to cover these initial expenses.

ARTICLE : 10 costs to consider when buying a home

5- Who pays the notary fees, the buyer or the seller?

Generally, the notary is chosen by the buyer, who is also responsible for paying the fees. The amount may vary depending on the complexity of the file and the notary's firm.

On the other hand, the seller is also responsible for fees incurred by the notary on their behalf, including:

- The fees for publishing the discharge in the Land Register

- The fees for obtaining official municipal and school tax statements

- The fees for obtaining the statement of common expenses (for a condominium)

- The title insurance premium (if applicable)

- Bank transfer fees (to pay the real estate broker, location certificate, outstanding taxes, etc.)

- Trust account management fees for the seller's portion of the transaction

- Copies of deeds

- Etc.

ARTICLE : What happens at the notary's office when you buy a property?

6- Is mortgage pre-approval mandatory?

No.

However, it allows you to determine the maximum mortgage amount you could qualify for, estimate your monthly payments, and lock in an interest rate for a period of 60 to 130 days (depending on the lender). Above all, a pre-approval is a powerful bargaining chip with sellers and can make all the difference in getting your offer accepted, as it demonstrates the seriousness of your intent.

ARTICLE : Demystifying the mortgage

1.Government of Canada. How much you need for a down payment, [Online]. [https://www.canada.ca/en/financial-consumer-agency/services/mortgages/down-payment.html] (Accessed Mars 9, 2026).